Most founders pick their market, then hope for the best exit. That is backwards. The exit determines the market.

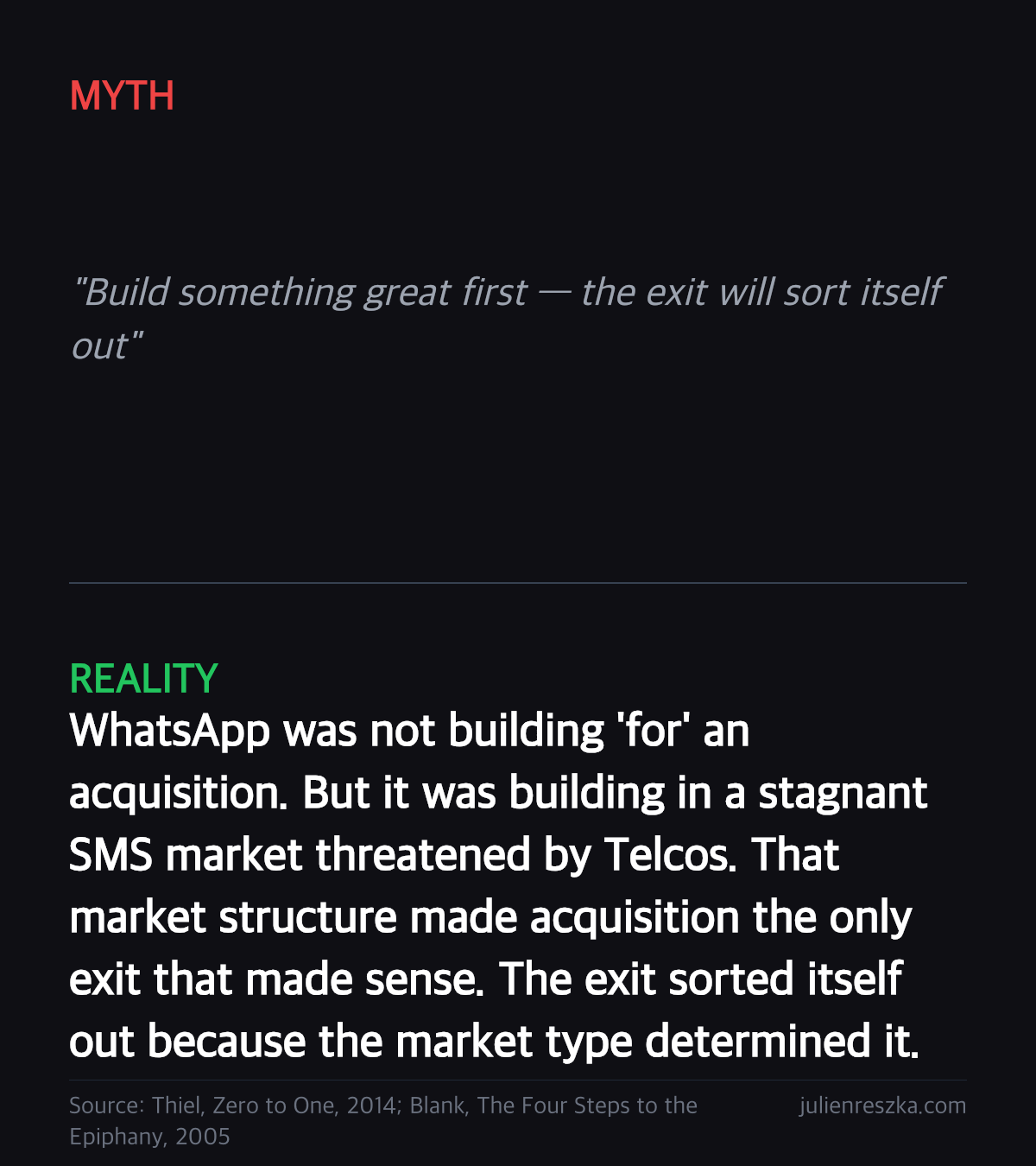

WhatsApp threatened Telcos' SMS revenue in a stagnant market → acquired for $19B. Uber rode a fast-growing market by scaling faster than supply and demand could naturally clear → IPO. Basecamp stayed profitable in a high-margin SaaS niche, never raised a Series A → founders exited on their own terms via secondary.

Three exits. Three market types. Three completely different playbooks:

- Acquisition in stagnant markets: open the 10-K of the incumbent you want to threaten. Find the risk factor that names what could kill them. Build that product.

- IPO in fast-growing markets: growth rate is the only metric that matters. Optimise for margin too early and you cede position. Whoever holds the most land when the market matures wins.

- Profitable exit in high-margin markets: spend less than you earn from month two. Own the equity. Exit via secondary sale or dividends, with no roadshow and no lockup.

The three market types are not interchangeable. Scaling in a stagnant market funds the incumbent's comfort. Optimising for margin in a land-grab hands the market to whoever is still burning capital. Burning capital to grow fast in a high-margin niche is just paying to lose equity.

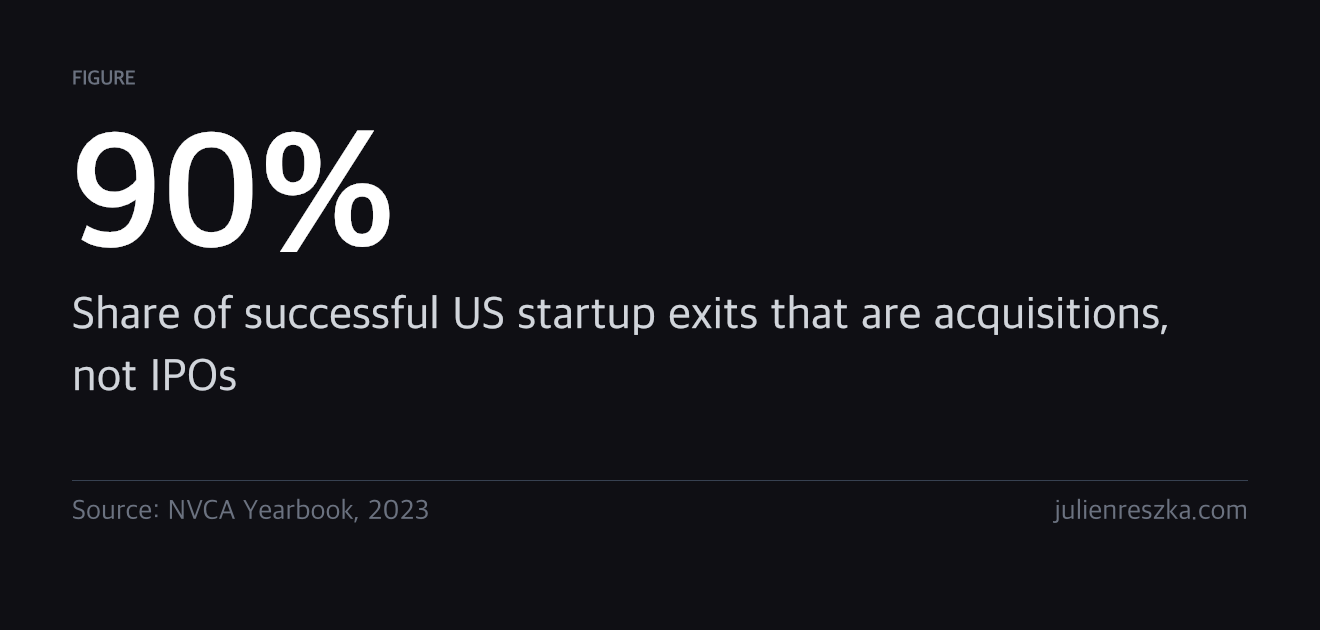

90% of successful US startup exits are acquisitions, not IPOs. Most founders spend their time optimising for a public listing that will not happen, in a market structure that does not support it.

Discussion

We spent two years building for an IPO in what is clearly a stagnant market. Wrong exit for our market type, full stop. The 10-K trick alone is worth sharing this everywhere.

Same. We were burning capital to scale when the market rewarded disruption. The exit choice would have told us that from the start.

The 10-K risk factor trick is the most actionable startup advice I've read this year. We found three disclosures from a €2B incumbent last month that map to what we're building. Now I know that's not luck, it's the correct move.

We will exit via acquisition because our market is stagnant: three large players with locked-in enterprise contracts and no appetite to rebuild their data pipeline tooling. We are the thing they will buy rather than build.

This is the cleanest answer to the sentence I've seen. You've already identified the acquirer profile. Most people haven't even done that.

We will exit via IPO because our market is fast-growing. Logistics automation for SMEs in Southeast Asia, TAM expanding 30% year on year. The only question is whether we can hold position long enough for the market to mature around us.

Honest answer: I cannot complete it. We picked a market first and assumed the exit would follow. This post is the first time I've seen that framed as a mistake rather than just 'normal founding'. Rewriting our deck this week.

Same place six months ago. The sentence is uncomfortable to write because it forces a real answer. That discomfort is exactly the point.

The three buckets are clean in theory but markets don't arrive pre-labelled. Most founders I know couldn't correctly identify whether their market was stagnant or fast-growing until eighteen months in, and by then the strategy was already set. Pre-choosing your exit before you understand your distribution feels like picking a wedding venue on a first date.