The Armey Curve proposes an inverted-U relationship between government spending as a share of GDP and economic growth. The logic is intuitive: too little government and you have no property rights or courts; too much and you crowd out private investment. Somewhere around 20-30% of GDP is the sweet spot.

The data does not support a sweet spot.

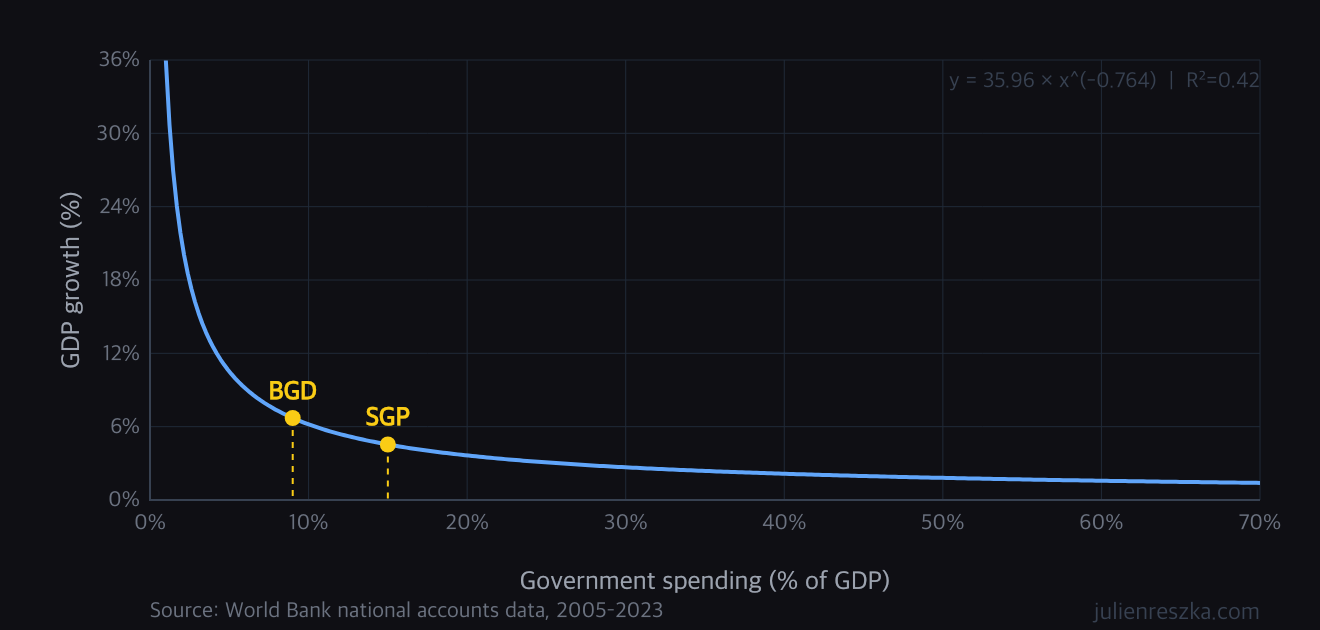

Cross-country World Bank data from 113 countries over 2005-2023 fits a power law better than any quadratic. R2=0.42 for the monotonically decreasing power law versus R2=0.39 for the traditional Armey curve. The relationship is not U-shaped. It just goes down.

Some reference points:

- Singapore: government spending around 15% of GDP, persistent above-average growth over decades

- Bangladesh: around 9%, one of the fastest-growing economies of the past two decades

- South Korea built its high-growth phase with government under 20%

- High-spending OECD economies consistently underperform on growth relative to their income level

No sweet spot appears at 20%, 25%, or 30%. The curve keeps falling.

This answers how much but not on what. If spending reliably slows growth, the question becomes when the brake is worth pulling.

Two conditions must both be met for an intervention to be justified.

First, the activity must impose a net wealth loss on external parties (people who bear cost without being participants in the transaction), summed across all capital kinds: produced, human, natural, knowledge, and institutional. A factory that poisons a river fails this test. A business that outcompetes a rival does not, because the rival was a voluntary participant in the market.

Second, the intervention must be cost-effective: the deadweight loss from the regulation, plus enforcement cost, plus the probability of regulatory capture multiplied by its expected damage, must be less than the external wealth loss it prevents. A regulation that costs more to enforce than the harm it stops fails this test even if the harm is real.

Activities that satisfy both conditions are genuine negative externalities:

- Pollution that degrades shared resources beyond self-repair rates

- Resource extraction that exceeds regeneration, destroying future productive capacity

- Systemic financial risk, where institutions privatize gains and socialize losses

Activities that fail one or both conditions (licensing requirements that protect incumbents, subsidies that redirect investment without correcting a price signal, spending programs that transfer wealth without addressing an external cost) slow growth without a welfare justification.

The two-condition test does not require a macroeconomic model. It requires identifying who is bearing cost they did not choose to bear, across what kinds of capital, and whether the intervention is cheaper than the damage it prevents.

The formal criterion is implemented in shouldBreak.js, including the certainty-equivalent pricing rule, the trustworthiness gate, and the required insurance coverage calculation.

Discussion